While the China Aviation MRO Logistics Market is positioned for rapid growth and remarkable opportunity, the path ahead also involves multiple challenges. Effective strategic planning, technological adoption, and operational discipline will be critical for stakeholders to succeed in this evolving market.

One of the principal challenges lies in the complexity of aviation supply chains. With diverse aircraft types — narrow-body, wide-body, business jets, military planes — the variety of spare parts, components, and maintenance kits is vast. Ensuring accurate inventory, timely procurement, secure storage, and reliable distribution across multiple hubs is not trivial. Mismanagement can lead to delays, grounded aircraft, or regulatory non-compliance. Therefore, logistics providers must invest in advanced inventory management systems, robust forecasting, and demand planning to ensure readiness and accuracy.

Another challenge is cost pressures and operational efficiency. Maintaining warehouses, ensuring compliance with aviation standards, and providing rapid distribution — especially in a country as geographically large as China — can be expensive. Smaller logistics providers may find it difficult to meet these demands without significant capital investment. Furthermore, as airlines push for cost optimization, they may expect logistics providers to deliver high-quality services while keeping costs competitive, squeezing margins.

Regulatory and safety compliance also add complexity. Aviation parts and maintenance operations are tightly regulated. Logistics providers must ensure traceability, quality control, certification, and adherence to maintenance standards — especially for military and commercial aircraft. This demands rigorous quality assurance, documentation, and adherence to stringent protocols, which can complicate supply-chain workflows and add overhead.

Beyond these, another challenge includes supply-chain disruptions, whether due to global supply volatility, geopolitical effects, or manufacturing bottlenecks. For critical components — especially for newer aircraft models — delays in manufacturing or export can significantly impact maintenance schedules. Logistics providers must build resilience, diversify supplier bases, and maintain buffer inventories — at the cost of increased inventory holding and capital tie-up.

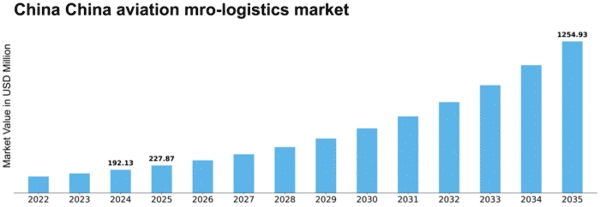

Yet, despite these challenges, opportunities abound. As projected, the China Aviation MRO Logistics Market Size is expected to reach USD 1,254.93 million by 2035. Strategic investors and providers who adopt modern logistics practices — such as predictive demand forecasting, automated inventory systems, centralized distribution hubs, and data-driven supply-chain analytics — can capture significant market share.

Additionally, the increasing adoption of digitalization, predictive maintenance, and real-time inventory tracking will strengthen the role of logistics providers. As airlines and MRO operators shift towards data-driven maintenance scheduling and lean supply-chain models, reliable logistics networks will be critical to deliver parts just-in-time, reduce holding costs, and ensure aircraft uptime.

Finally, expanding infrastructure — new warehouses, specialized MRO hangars, logistic centers near major airports — plus strategic partnerships between airlines, OEMs, and logistics providers will underpin future growth. As China’s aircraft fleets expand and flight hours grow, the reliance on robust, efficient, and responsive aviation MRO logistics will become central to the country’s aviation ecosystem.

In conclusion, while the path ahead includes complexity and cost pressures, the long-term outlook for the China Aviation MRO Logistics Market remains strong. Providers who leverage technology, build robust supply-chain networks, and deliver efficiency and compliance will likely emerge as key enablers of China’s aviation growth story.

Related

Discover More Research Reports on Aerospace & Defense By Market Research Future:

US Aerial Refueling Systems market